Health Care & Wellness

PDAB Implementation Challenges Slow State Drug Cost Efforts

June 8, 2026 | Mary Kate Barnauskas

September 4, 2025 | Brock Ingmire

Key Takeaways:

In 2025, medical debt reform became a flashpoint in both statehouses and federal courts as policymakers wrestled with how best to protect consumers from the financial burdens of health care. During the Biden Administration, advocates had pinned their hopes on federal action through the Consumer Financial Protection Bureau (CFPB). But with a major court decision striking down a Biden-era rule and the Trump administration unlikely to defend it, states have and are likely to continue to step in to shape the future of medical debt policy even as their efforts face legal uncertainty.

In January 2025, just before leaving office, the Biden administration finalized a CFPB rule removing medical debt from consumer credit reports. The rule barred credit reporting agencies from listing medical debt on consumer reports and prohibited lenders from factoring medical debt into underwriting decisions. The agency argued that medical debt was an inadequate measure of creditworthiness, often stemming from emergencies, billing errors, or disputes with insurers. By CFPB estimates, the rule would have erased $49 billion in reported debt for 15 million individuals and raised their credit scores by an average of 20 points, potentially expanding access to more stable housing and financial stability.

But in July 2025, a federal district court in Texas vacated the rule. The court ruled that the CFPB had exceeded its authority under the Fair Credit Reporting Act, which explicitly permits medical debt to appear on reports. It also found the agency failed to provide sufficient justification under the Administrative Procedure Act. Importantly, the ruling emphasized that federal law preempts state attempts to ban reporting of medical debt, casting doubt on state-level reforms. With the rule nullified, credit bureaus are again free to report medical debt, and the Trump administration has shown no interest in appealing or reviving the policy.

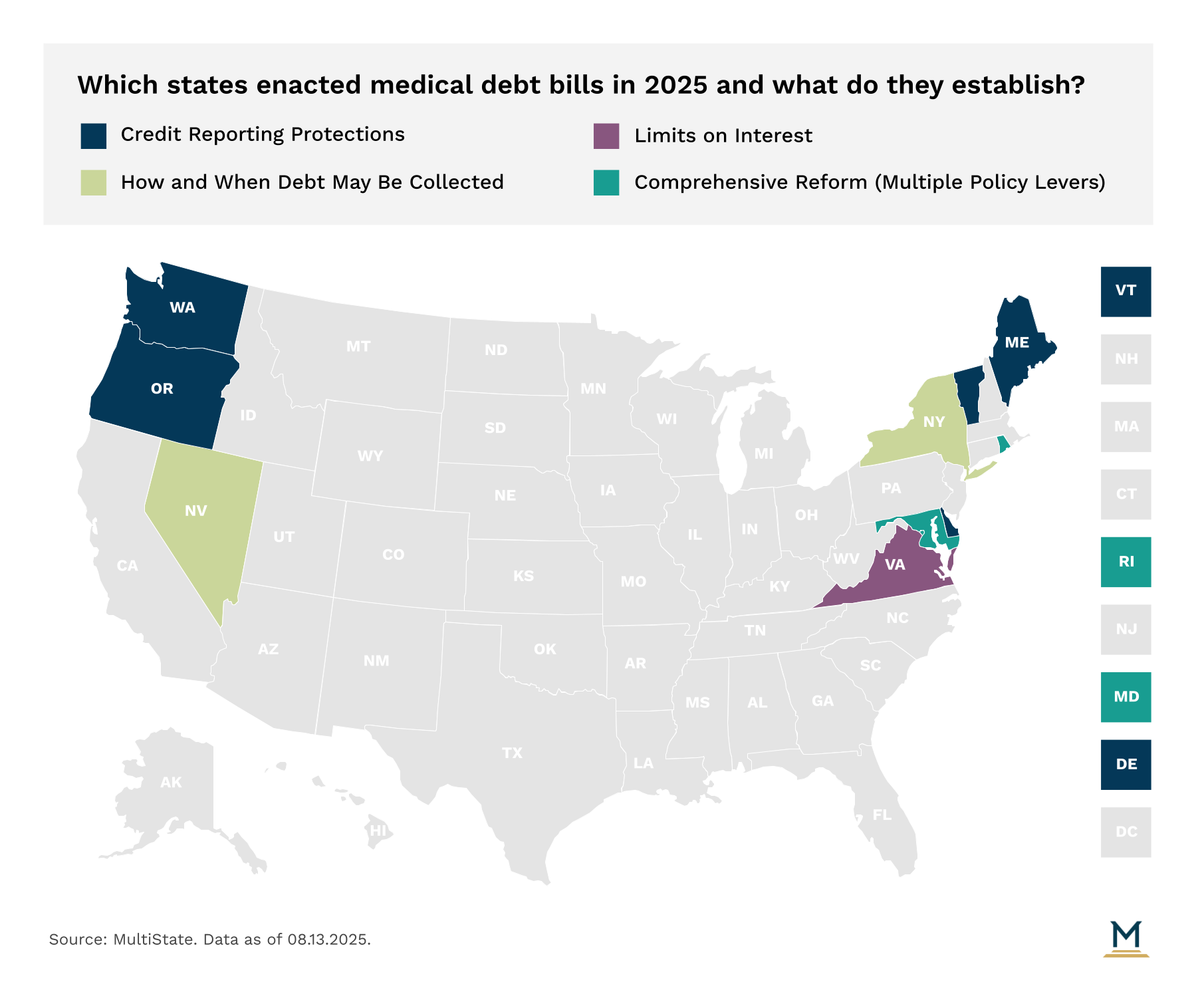

Even before the Texas decision, states had begun moving aggressively. In 2025, more than 123 bills across 38 states were introduced to address medical debt. At least 30 passed one legislative chamber, and 14 were enacted into law across 10 states.

The most common reforms fell into four categories:

Prohibits the reporting of medical debt information to consumer reporting agencies or for consumer reporting agencies from reporting that information on consumer reports (Delaware, Maine, Maryland, Oregon, Rhode Island, Vermont, and Washington).

Establishes limitations on how interest may be applied to medical debt in varying situations [Maryland (SB 981/HB 268), Rhode Island (HB 5235/SB 172), and Virginia].

Prohibits providers and contracted entities from either collecting debt in certain circumstances or narrowing the scope of what qualifies as medical debt to collect [Maryland (SB 981/HB 268), New York (S.753/A.5235), and Nevada].

Authorizes hospitals to sell medical debt of patients to a governmental unit or entity for purposes of debt cancellation (Maryland).

Maryland led the way with the most comprehensive package. Its new laws ban credit reporting of medical debt, prohibit hospitals from charging interest without a court order, block lawsuits over debts under $500, prevent collections within 240 days of billing, and authorize debt sales for cancellation. While many of these provisions are expected to stand, the credit reporting ban may not survive federal preemption challenges.

As 2025 closes, Michigan and North Carolina are considering additional reforms. Michigan’s SB 95 would prohibit hospitals from collecting debt if they are not compliant with federal hospital price transparency rules, though its passage is uncertain due to ties with a controversial 340B reform bill. North Carolina’s SB 316 would prevent hospitals from sending debts to collection agencies unless patients receive itemized bills, reflecting broader transparency efforts.

Looking forward, states are expected to pivot from outright bans on credit reporting—now on shaky legal ground—to alternative reforms. Interest rate caps are likely to expand, particularly in Democratic-led states. Meanwhile, Republican-controlled legislatures may pursue policies linking debt collection to hospital transparency and financial assistance standards. The result will likely be a patchwork of state protections, with varying degrees of durability depending on how courts interpret federal preemption.

StateVitals is the leading resource on how state governments are shaping healthcare policy and transforming care and delivery, brought to you by MultiState’s Health Care Policy Practice. MultiState’s policy and advocacy professionals are uniquely positioned to give you and your organization the big-picture view on state health policy reform, plus the latest trends on how policymakers are thinking about healthcare and similar emerging issues. Learn more about StateVitals, or schedule a demo here.

June 8, 2026 | Mary Kate Barnauskas

May 12, 2026 | Mary Kate Barnauskas

April 1, 2026 | Mary Kate Barnauskas