Technology & Privacy, Tax & Budgets

How States Are Taxing Digital Goods, Social Media, and Targeted Advertising

July 30, 2026 | Andrew Jones

August 5, 2025 | Morgan Scarboro

Key Takeaways:

This is an excerpt from our report on the state impacts of the One Big Beautiful Bill Act (OBBBA). To read the full report, download it here.

On July 4, 2025, President Trump signed H.R. 1, the One Big Beautiful Bill Act (OBBBA), into law. The bill contains hundreds of provisions on healthcare, tax, and spending priorities. Many of these provisions will directly or indirectly affect the states, their spending decisions, and their budget health.

Many of the tax provisions in the bill are actually extensions or modifications of the 2017 Tax Cuts and Jobs Act (TCJA). Here are some of the key points.

Restores full expensing for domestic research & experimental expenditures, with some retroactivity allowed for small businesses

Restores full interest expense deductibility under Section 163(j)

Raises Section 179 expensing limits for equipment purchases

Extends full bonus depreciation through 2028

Modifies TCJA-era international tax provisions such as GILTI and FDII

Repeals or reforms many Inflation Reduction Act (IRA) green energy credits

Temporarily increases the State and Local Tax (SALT) deduction

Makes permanent the 199A (pass-through business) deduction

Makes permanent the TCJA individual income tax rates

Exempts a portion of tip income from federal income taxation

Exempts a portion of overtime pay from federal income taxation

The impact of every federal tax change on states depends on conformity. Essentially, states piggyback off of the federal Internal Revenue Code (IRC) for a variety of policy and administrative purposes. However, states differ in their conformity approaches. Some states automatically adopt new federal changes without the legislature having to pass a bill, but others have a static conformity date and must proactively pass legislation updating the version of the IRC they conform to. Further, states rely on different calculations in the federal code for their starting point. Therefore, it’s impossible to broadly predict how the OBBBA will impact all states.

While there are many tax policy changes in the bill at the federal level, most of those changes would require states to proactively conform to the updated Internal Revenue Code (IRC) provisions, so they will not experience “automatic” revenue losses. The primary tax reduction that will broadly flow through to states is the deduction for interest on auto loans.

An early Tax Foundation estimate predicted that if all states either automatically or proactively updated their conformity date to the current IRC, the tax changes would reduce state revenue by only $3.7 billion in aggregate in tax year 2026. This represents less than one percent of state individual income tax collections. However, some of these provisions, like an exemption for a portion of tipped wages and overtime pay, are politically popular. So if states went a step further and also enacted their own matching exemptions (for tips and overtime pay, as those would largely not be captured in conformity), the effect would be an annual aggregate reduction of $20.5 billion, 4.2% of state income tax collections.

The changes to research and experimental (R&E) expenditures will also impact states. Beginning in tax years after December 31, 2021, the TCJA required taxpayers to amortize certain R&E costs over five years for domestic research. However, the OBBBA restores the ability for taxpayers to immediately deduct these domestic expenses, or choose to amortize over at least five years. This choice is a welcome change for many business taxpayers. Thirty-nine states conform in some way to federal 174 treatment; however, states may need to issue guidance, particularly on the retroactive provisions.

The larger impacts on state budgets come not from tax policy changes, but changes to the way the federal government contributes to SNAP benefits and Medicaid costs. The Medicaid cost changes are discussed in detail in this report, totaling up to $1.02 trillion in reduced federal funding over ten years for states.

Changes to the Supplemental Nutrition Assistance Program (SNAP) will have significant cost implications for states. Previously, the federal government funded all of the benefit costs and split the administrative costs with states. However, beginning next year, states will begin paying 75% of administrative costs, and, beginning in 2027, states will be responsible for a portion of the benefit costs — up to 15% depending on states’ error rates. Even without accounting for increased administrative costs, the benefit cost shift could cost states hundreds of millions per year if states decide to continue funding the program at its current level. Although policymakers will need to address these funding questions, they have some time to consider options and funding mechanisms as these changes will take several years to phase in.

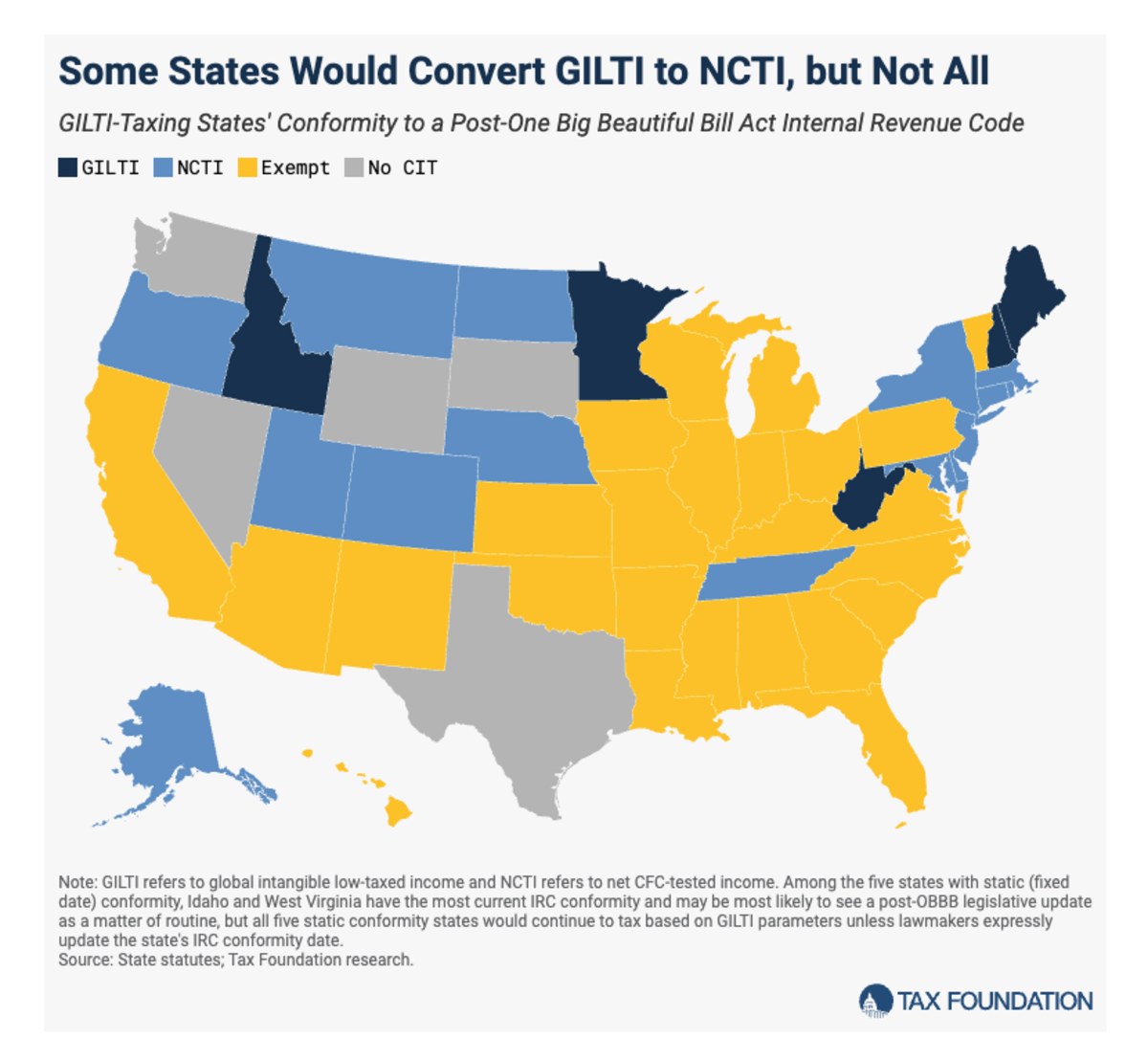

Policymakers will need to consider changes to some of the international provisions. States should reconsider their treatment of Global Intangible Low Taxed Income (GILTI), now renamed to Net CFC-Tested Income (NCTI). At the time of its enactment, GILTI was intended to be a form of a minimum tax on certain types of foreign earnings. Most states do not tax a material portion of GILTI for a variety of policy and constitutional reasons regarding state tax treatment of foreign income.

Image credit: Tax Foundation.

However, the bill makes changes to sourcing and the treatment of certain deductions and credits under NCTI. As a result, states that incorporate NCTI into their tax base will now take an even more aggressive, complex approach to taxing international income. When overlaid with conformity considerations, the landscape of international taxation at the state level becomes incredibly complex for multinational corporations to follow. It is not possible for states to provide the same necessary incentives and concessions as the federal government when it comes to taxing foreign income, so state policymakers who have previously coupled to GILTI must reconsider.

This article appeared in our Morning MultiState newsletter on August 5, 2025. For more timely insights like this, be sure to sign up for our Morning MultiState weekly morning tipsheet. We created Morning MultiState with state government affairs professionals in mind — sign up to receive the latest from our experts in your inbox every Tuesday morning. Click here to sign up.

July 30, 2026 | Andrew Jones

July 17, 2026 | Andrew Jones

June 24, 2026 | Andrew Jones