Tax & Budgets

State Revenue Challenges Mount Despite Record Rainy Day Funds (State Fiscal Health Update)

June 24, 2026 | Andrew Jones

March 30, 2026 | Katherine Tschopp

Key Takeaways:

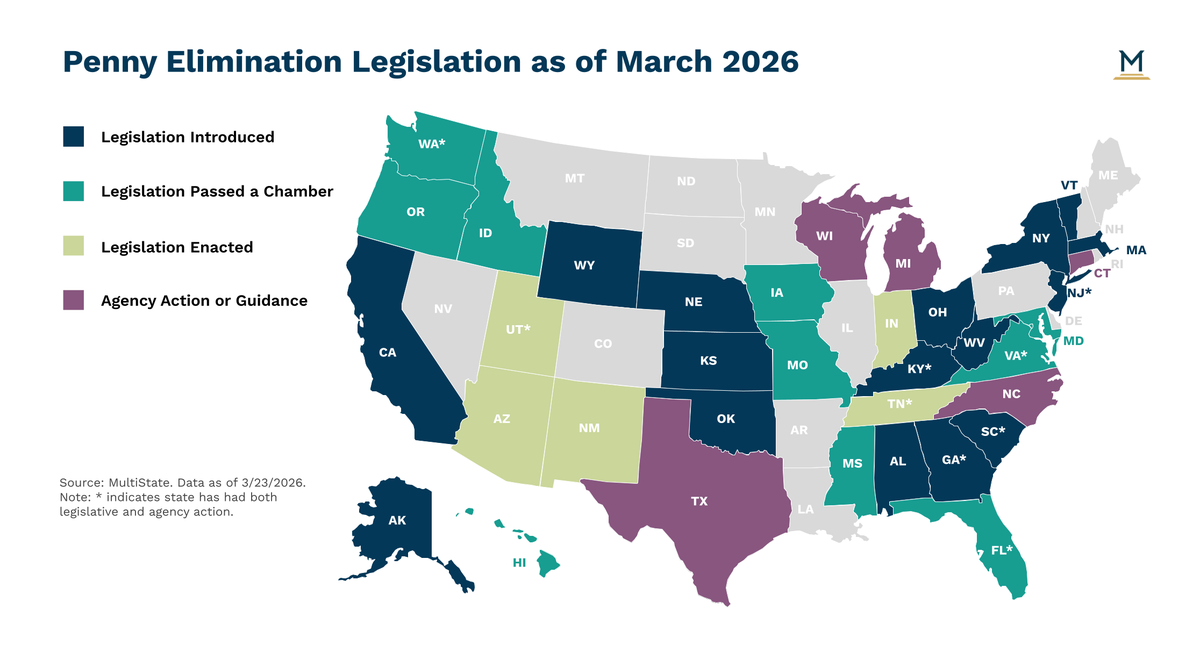

Last month, we officially marked one year since President Trump announced plans to eliminate the penny in a social media post. Retailers and consumers began to feel the effects of halted penny production in the fall, and turned to lawmakers for a roadmap as the coin is phased out. Although Congress introduced two “Common Cents” bills (USA HR 3047 and USA S 1525) in 2025 — proposing price rounding policies for cash payments and small change transactions — neither bill has advanced beyond the introduction stage. Price rounding applies only to cash transactions (not credit card transactions), where exact change is no longer possible without the penny. Utah’s Division of Consumer Protection was the first state agency to issue guidance on cash rounding in November, with a growing number of state legislatures and agencies following suit to address federal inaction.

What originally started as recommending specific price rounding strategies as a result of penny elimination (e.g., agency guidance in Connecticut and Kentucky) quickly expanded. Elsewhere, state agencies have focused less on prescribing a uniform, or any, approach and more on addressing the tax implications of rounding. Under these new rounding policies, if your purchase is for $0.98 and the retailer rounds that up to $1, do you pay sales tax on the 98 cents or the dollar? State revenue agencies have started to answer that question.

Many state Departments of Revenue emphasized that retailers and merchants must still collect and remit the correct amount of sales tax, regardless of the rounding method they adopt. For example, the Departments of Revenue in Florida, Georgia, and Michigan have issued notices requiring that retailers must complete standard sales tax calculations before applying any rounding. These interim guidance notices generally leave the choice of rounding method to the retailer’s discretion, while reinforcing compliance with existing tax obligations.

Some agencies have gone further by issuing guidance on additional types of taxes. The Wisconsin Department of Revenue addressed property tax collection in a post-penny environment, clarifying that amounts may not be rounded to the nearest nickel and that the exact tax owed must be collected. In Washington, the Department of Revenue has announced that it will not, for now, enforce business and occupation (B&O) tax liability on any gains resulting from rounding, and will instead revisit enforcement in its final guidance. Like the federal government, most state agency activity appears to defer final decisions on penny elimination price rounding methods to their legislatures.

We see the same patterns in the first handful of enacted price rounding laws. As of March 23, governors in five states have signed price-rounding bills into law: Arizona (AZ HB 2930), Indiana (IN SB 243), New Mexico (NM HB 291), Tennessee (TN HB 1744), and Utah (UT HB 597). In Arizona and Tennessee, the new laws set price rounding methods for cash payments, so long as the rounding occurs after the sales tax is calculated and applied. Indiana’s newly enacted law establishes the Canadian price rounding method, rounding up or down to the nearest nickel based on the second decimal place of the total for retail transactions. Additionally, the Indiana law requires cash payments of state and local taxes to always be rounded down to the nearest nickel. New Mexico’s law authorizes the Department of Revenue to allow or require taxes and motor vehicle fees to be rounded to the nearest nickel.

Most of the more than 55 introduced state penny elimination bills include language that would explicitly require the sales tax to be calculated according to the pre-rounded transaction total and prohibit any rounding strategy from affecting the sales tax amount. However, like the agency guidance and enacted legislation, price rounding bills also propose to regulate rounding for specific tax payments. An Ohio bill (OH HB 737) would require any cash payment for a tax, toll fee, fine, or other charge to a state or local jurisdiction to be rounded to the nearest nickel. Contrary to Wisconsin’s guidelines on property tax payments, New York Assemblymember Paula Kay (D) introduced legislation (NY A 10207), which would require collecting officers to round cash payments of real property tax and interest to the nearest nickel.

The common thread across agency guidance, enacted laws, and pending legislation is a shared instinct to protect sales tax calculations from rounding distortions while leaving the actual rounding method largely to retailers or future legislative action. Some lawmakers are extending rounding provisions beyond sales tax to other tax payments as states look to protect revenue streams strained by federal budget cuts under OBBBA (US H.R. 1). As more states move to fill the federal vacuum, the bigger question may be whether Congress eventually sets a uniform national standard or whether the patchwork of state approaches becomes the permanent framework.

Tax policy can be one of the most challenging areas for government affairs executives. MultiState’s team understands the issues, knows the key players, and helps you effectively navigate and engage. We offer a customized, strategic solution to help you develop and execute a proactive multistate tax legislative agenda. Learn more about our Tax Policy Practice.

June 24, 2026 | Andrew Jones

April 6, 2026 | Jose Perez

March 30, 2026 | Morgan Scarboro, Kim Miller