Compliance

A Guide for Understanding Time Sensitive Lobbying Reports and Deadlines by State

July 2, 2026 | Ben Zuegel

Key Takeaways:

The sales tax is a tax on transactions based on the value of the good or service that was purchased. All but five states impose a sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon. Due to the varying statutes, rules, and guidance provided by each state, staying in compliance with tax laws may be difficult.

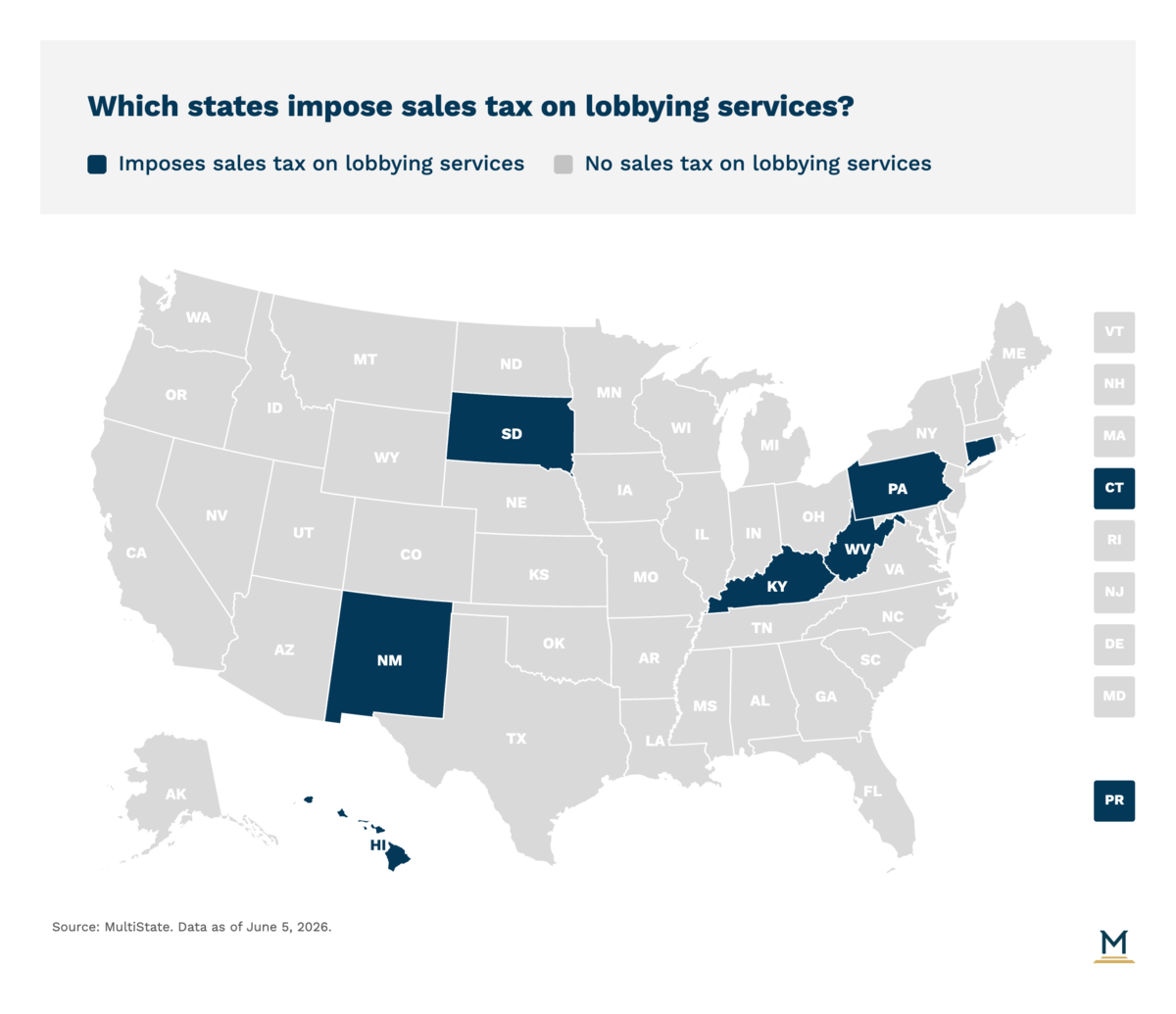

As of now, seven states and one territory impose a sales tax on lobbying services: Connecticut, Hawaii, Kentucky, New Mexico, Pennsylvania, South Dakota, West Virginia, and Puerto Rico. The specifics of the tax on lobbying services differ from state to state.

For instance, in Hawaii, Kentucky, and Connecticut, which impose a tax on lobbying services at a rate of 4%, 6%, and 6.35%, respectively, the sales tax is imposed by the state only.

New Mexico, South Dakota, and Pennsylvania include an added layer of complexity by authorizing local jurisdictions to impose a sales tax of their own on lobbying services. Rates imposed by local jurisdictions can differ from one city or county to another within the same state. Including the local sales tax rate, New Mexico imposes a sales tax rate between 5.125% to 8.9% depending on the jurisdiction. Pennsylvania imposes a sales tax rate between 6.0% to 8.0%. South Dakota imposes a sales tax rate between 4.5% to 6%.

West Virginia takes a nuanced approach to taxing lobbying services. While lobbying is generally subject to a 7% tax, a licensed attorney that provides professional legal services to a specific client, such as legislative drafting, or written analysis of legislation, is exempt from the sales tax.

While Tennessee does not impose a sales tax on lobbying services, the state imposes a $400 professional privilege tax annually on registered lobbyists. And while certainly not a U.S. state or territory, Canada imposes a 13% tax on lobbying services.

While only a handful of states tax lobbying services, in recent years states such as Louisiana, Nebraska, and Maryland have sought to expand their sales tax base to include lobbying services. So far those attempts have failed, but will likely pop up again. Likewise, efforts to broadly expand the sales tax base, which would sweep in lobbying services as a taxable service, have also fallen short. For instance, IN HB 1288 was introduced in Indiana this past session but did not make it out of committee.

With about half of state legislatures adjourning their regular session, there are no active bills that specifically target lobbying services for taxation. However, Missouri has passed a constitutional amendment, which requires voters' approval, to expand the sales tax base (MO HJR 173). Likewise, legislation in Michigan (MI HB 5880) would broadly impose an excise tax on goods and services that are not currently taxed. State tax codes can change at a dizzying pace. With changes in law, the status of lobbying as a taxable service can change along with it, leading to increased costs for those looking to hire lobbyists.

Tax policy can be one of the most challenging areas for government affairs executives. MultiState’s team understands the issues, knows the key players, and helps you effectively navigate and engage. We offer a customized, strategic solution to help you develop and execute a proactive multistate tax legislative agenda. Learn more about our Tax Policy Practice.

Which states charge sales tax on lobbying services?

Seven states and one territory currently impose a sales tax on lobbying services: Connecticut, Hawaii, Kentucky, New Mexico, Pennsylvania, South Dakota, West Virginia, and Puerto Rico. The tax rates range from 4% to 8.9% depending on the state and local jurisdiction. Tennessee does not impose a sales tax on lobbying but charges a $400 annual professional privilege tax on registered lobbyists.

What is the sales tax rate on lobbying services in Pennsylvania?

Pennsylvania imposes a sales tax rate between 6.0% and 8.0% on lobbying services. The variation in rates is due to local jurisdictions being authorized to impose their own sales tax on top of the state rate, which can differ from one city or county to another.

Are there any exemptions to the sales tax on lobbying in West Virginia?

Yes, West Virginia exempts licensed attorneys who provide professional legal services to a specific client, such as legislative drafting or written analysis of legislation. While lobbying is generally subject to a 7% tax in West Virginia, this exemption applies when the services fall under professional legal work for a particular client.

Are any states currently trying to pass legislation to tax lobbying services?

Missouri has passed a constitutional amendment (HJR 173), which requires voters' approval, to expand the sales tax base. Michigan has legislation (HB 5880) that would broadly impose an excise tax on goods and services that are not currently taxed. Indiana introduced HB 1288 this past session but it did not make it out of committee.

Does New Mexico impose local sales tax on lobbying services in addition to state tax?

Yes, New Mexico authorizes local jurisdictions to impose their own sales tax on lobbying services in addition to the state tax. The combined state and local sales tax rate on lobbying services in New Mexico ranges from 5.125% to 8.9% depending on the jurisdiction.

July 2, 2026 | Ben Zuegel

July 1, 2026 | Ben Zuegel, Vinnie Cannamela

June 29, 2026 | Denisse Girón, Ahmed Zain